More than half a million workers are paying income tax on up to 60 per cent on the top chunk of their earnings, figures show – meaning they will lose the majority of their next pay rise to tax.

The number being caught in this punitive tax trap, which affects those earning between £100,000 and £125,140 a year, is higher than ever, according to analysis by the accountancy firm Bowmore Financial Planning.

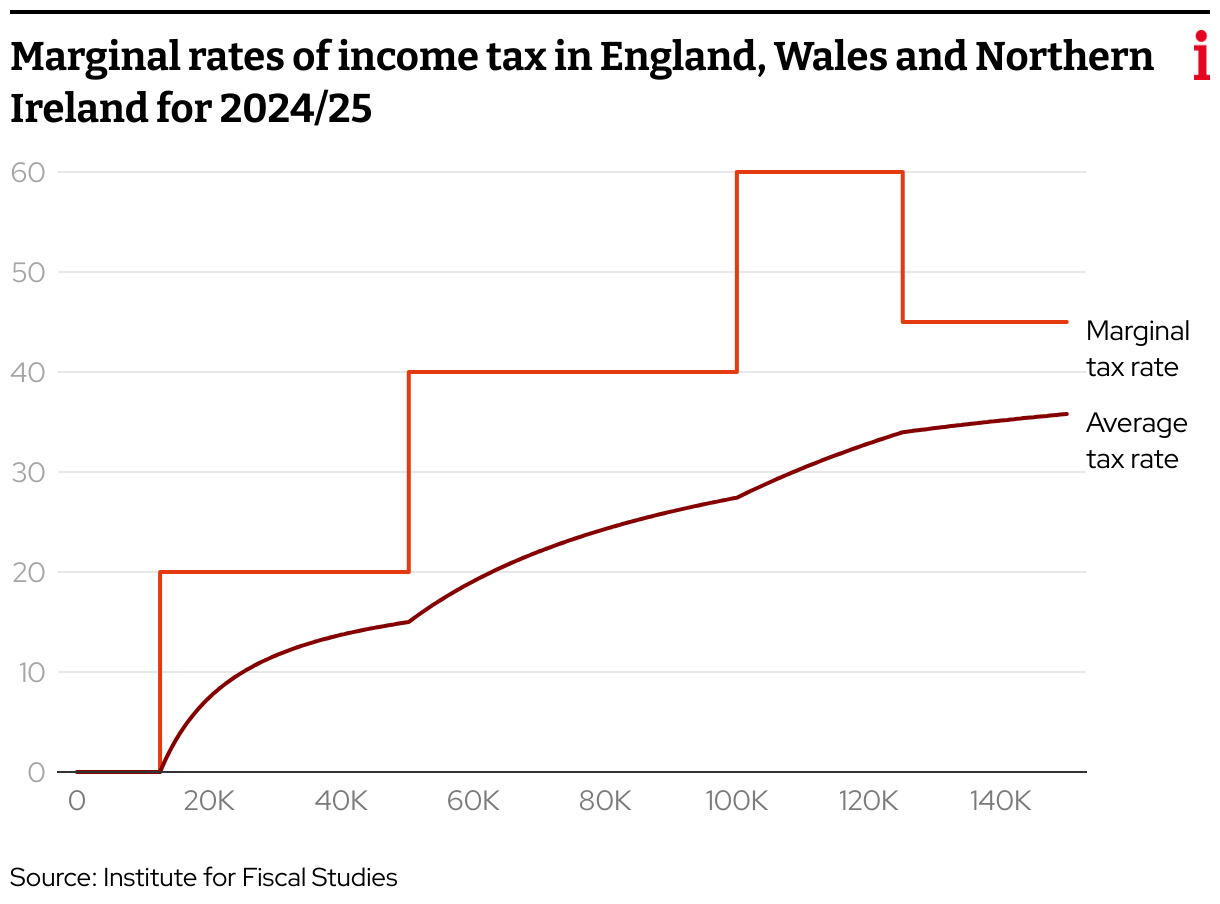

In England, Wales and Northern Ireland, the official top income tax rate is 45 per cent and applies to earnings above £125,140. But, thanks to a quirk in the system, you can pay a marginal tax rate (the actual rate paid on the next pound that you earn) of 60 per cent on earnings between £100,000 and £125,000.

This is because for every £2 you earn above £100,000, you lose £1 of your £12,750 personal allowance – the amount you can earn each year without paying any tax at all. By the time you earn £125,140, that allowance has been tapered away to nothing.

It means anyone caught in the trap pays 60p in tax on that part of their earnings, plus 2p of additional national insurance contributions, so they lose the majority of any increase to their pay between £100,000 and £125,140.

The number of taxpayers falling into this income range rose by 23 per cent from 436,000 to 537,000 between 2021-22 and 2022-23, according to a Freedom of Information request.

The figure today, however, is likely to be much higher after another year of frozen income tax thresholds.

Experts have called on the Government to take “urgent action to fix this inequality in the income tax system”.

Jason Hollands, managing director of Evelyn Partners, told i: “Of all the quirks in the tax system, the ‘60 per cent tax trap’ is by far and away the worst in my view as it both very punitive and horribly opaque.

“I’m afraid if this is left unaddressed, the number of people being hit by the 60 per cent tax trap is going to continue to skyrocket from here as nominal annual pay rises occur, while tax allowances and thresholds are set to remain frozen until at least April 2028 under the Government’s fiscal framework.”

One way to mitigate this “zone of painful taxation” for those whose earnings could be taken into this trap by a salary increase or bonus is to forgo these in lieu of an increase pension contribution, Mr Holland said. This is known as salary sacrifice and is worth exploring for anyone whose earnings are in this zone or on the cusp of entering it.

Thresholds have been frozen since 2020-21 and will remain so until 2027-28. The former chancellor, Jeremy Hunt, went one step further in April last year and cut the 45p additional rate threshold from £150,000 to £125,140.

In turn, millions of taxpayers have been dragged into higher tax brackets as inflation pushes up wages.

Parents in this income bracket can even lose money if their pay rises. Once a parent earns more than £100,000, they lose tax-free childcare and half the 30 hours a week of free care that is available for three and four-year-olds.

This tax break is worth up to £14,500 a year for someone with two children, creating an incentive for parents earning £99,000 to turn down a pay rise so they can hold on to these helpful benefits.

Mark Incledon, chief executive at Bowmore Financial Planning, said: “Reaching a six-figure salary has long been a major goal for a lot of people. We all understand that this comes with the obligation to pay more tax.

“Unfortunately, if HMRC takes 60p in every pound you earn above £100,000, the lure of getting there is a lot more limited.

“It only disincentivises people from working harder, being more productive and ultimately generating economic growth.”

A Treasury spokesperson said: “We are committed to keeping taxes on working people as low as possible while maintaining fiscal responsibility, that’s why we’ve pledged to not raise income tax, national insurance or VAT.

“We are a government of wealth creation and believe the best way to responsibly improve living standards is through economic growth by guaranteeing stability, stimulating investment, and reforming our planning and skills systems to unlock Britain’s potential.”

How the tax trap works – and two ways to beat it

Everyone gets an income tax-free allowance of £12,570. So if you earn £50,000 you only get taxed on £37,430 of it.

However once you hit £100,000 in earnings, the tax-free allowance of £12,570 gets gradually taken away (at the rate of £1 for every £2 you earn). That means the allowance is gone entirely by the time you reach £125,140 in income, so you get taxed on all of it.

If you earn £110,000, the £10,000 that’s above the £100,000 threshold is taxed at 40 per cent (costing you £4,000).

Plus you lose £5,000 of your personal allowance, meaning £5,000 more of your earnings also gets taxed at 40 per cent (costing you £2,000). So that extra £10,000 just cost you £6,000 in income tax – an effective 60 per cent tax rate. Here’s how you can beat the trap.

Pension contributions

- Contributing to your pension is the most straightforward way to lower your adjusted net income, either via salary sacrifice or through personal pension contributions.

- The main advantage of salary sacrifice is that because the pension contribution never actually forms part of your salary, you don’t need to do anything else to claim tax relief, and you also do not pay national insurance (NI) on that portion of your income.

- For someone who earns £125,140, the easiest way to avoid the 60 per cent rate is to pay £25,140 into a pension via salary sacrifice, which would move them below the £100,000 threshold straight away and also save on NI.

Charity donations

- Charity donations through Gift Aid also help reduce your income tax burden, although they work a bit differently because they entail giving money away rather than moving it to a pension where it grows tax-free.

- When you make a charity donation with Gift Aid, the first 20 per cent of tax relief goes to the charity, and if you pay the higher rate of income tax you can then claim back the rest in your self-assessment.

- For example, if you earn £125,140 and make a net charitable donation of £20,112, thanks to Gift Aid, the charity will receive £25,140. You can then claim back the remaining £10,056 you paid in taxes through your tax return.